NEWS: A MESSAGE TO THE PROCESSORS WHO UNDERPAY ON BASE PRICE AND THEN ‘TOP-UP’ WITH A BONUS

– YOU’RE NOT FOOLING US!

It is that time of the year when dairy farmers would be normally be expecting to be enjoying the fruits of their Summer and preparing for the Winter ahead. Bills incurred during the Spring will be paid back with the expectation that all fodder would be in or on the way in. As discussed throughout this newsletter (and indeed the country), the drought has played havoc with many farmers looking at fodder deficits of up to 50% and significant merchant and Co-op bills to boot. Cashflow is extremely tight at presentand grass growth is still slow in many parts of the country. I won’t be alone in hoping that we can get the perfect weather this Autumn so more fodder can be harvested and grass can grow longer. That said, and as always, this article will focus on where the markets are going, where they have been, and we’ll try to throw some light on what’s likely to be in store over the coming months.

As discussed throughout this newsletter (and indeed the country), the drought has played havoc with many farmers looking at fodder deficits of up to 50% and significant merchant and Co-op bills to boot. Cashflow is extremely tight at presentand grass growth is still slow in many parts of the country. I won’t be alone in hoping that we can get the perfect weather this Autumn so more fodder can be harvested and grass can grow longer. That said, and as always, this article will focus on where the markets are going, where they have been, and we’ll try to throw some light on what’s likely to be in store over the coming months.

Cashflow is extremely tight at presentand grass growth is still slow in many parts of the country. I won’t be alone in hoping that we can get the perfect weather this Autumn so more fodder can be harvested and grass can grow longer. That said, and as always, this article will focus on where the markets are going, where they have been, and we’ll try to throw some light on what’s likely to be in store over the coming months.

SUPPLY

Growth in the supply of milk from the key producing regions (EU, NZ and US) accelerated in April and May, following lower than expected production during the first three months of 2018. 60% of that additional milk came from the EU28, with growth recorded for the US and New Zealand as well. In total, milk production from these regions is expected to be 1.5% higher in 2018 than last year, equivalent to an additional 4.3 billion litres. At the end of May, 53% of this expected 2018 growth had already been accounted for, with cumulative production 2.3bn litres higher than at the same time last year, according to ADHB. The latest milk production figures for July released by the Central Statistics Office in the last week of August underline graphically the effect the drought conditions had on dairy farms this summer. Irish milk production fell almost 27m litres in July 2018 compared to July 2017, this is a fall of 3.1% and reflects the immediate ‘knock-ons’ of the extreme weather and challenges around adequate feed and grass over the period. But that fall in supply is likely to be replicated across the EU and beyond and will have a positive impact on prices as the extent of the fall in milk produced works its way through the chain.

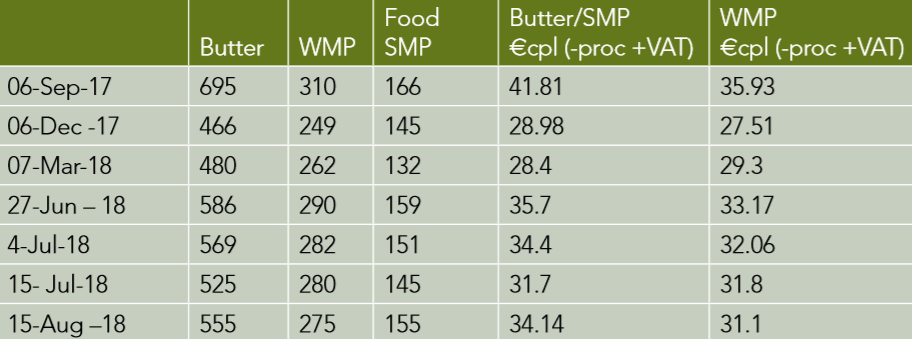

Prices on European wholesale markets have increased over the last number of weeks with returns for the Butter/SMP mix running at almost 35cpl and WMP over 32cpl. The fact is that revenues are being eaten-up by the increased costs associated with the drought and fodder challenges but that doesn’t detract from the imperative of getting the highest prices possible from the marketplace as we confront increased costs for the remainder of 2018 and into 2019. The current dominant question is how accurate those annual growth expectations will turn out to be? The recent poor grazing conditions across much of the EU will certainly have a restrictive effect on volumes, which could well bring the totals back in line with the EU Commission’s original expectations. All farmers across Ireland know the supply pattern on their farm for 2018, working forwards from the harsh cold dip in March to the drought affects of the Summer.

DEMAND

EU exports in the first five months of 2018 increased in volume for SMP (+4%), cheese (+1%) and whey powder (+1%). By contrast, decreases have been observed for WMP (-9%), butter (-5%) and butteroil (-2%). Total EU exports in this period, expressed in milk equivalent, would have been 2% below last year, while the value of these exports has decreased by -8%.

China is still the main global importer of butter, WMP and whey powder and increased its dairy import volumes in the first three months of 2018 – which, unfortunately, are the latest figures we have. Overall, global demand remains solid but slowed after a solid first 4-month period with higher market prices then impacting slightly. Trade wars and nervous market sentiment are also creating uncertainty with jittery price movements and the sale of SMP from India on the world market as well as the 100,000 tonnes sold from EU intervention also had to have had an effect.

PRICE

On the world market, prices had generally increased from January to April. Butter had taken a fall in the last months of the 2017 along with the powders only to gain back some of the momentum from March through June. After that, the momentum stalled but the last couple of weeks have seen a new move upwards across all combinations – albeit with another slight dip – as shown in Dutch Quotation table (Table 1). As always, we must take our direction from what was sold and at what price, and it is the Ornua PPI that accurately fulfills that criteria. The return for July was extremely encouraging at 32.1 cpl. and ICMSA expected all milk

purchasing processors to ‘step up’ and pay this as a minimum Base Price. The association does not accept increasingly common practice that has Co-ops paying a Base Milk Price that is below that of the Ornua PPI which is then ‘topped up’ by a cent or two on grounds of ‘Hardship’ or ‘Loyalty’. We reject the idea that paying any element of a proper, market-derived milk price can be ‘discretionary’ or at the whim of a processor’s management. We are convinced that farmers want to be paid

a proper price for their milk because that was what it was worth – not ‘at the whim’ of the processor who they were supplying.

We reject the idea behind this division of farmer milk price into ‘Base’ and ‘Bonus’ components with the former element invariably lower than the Base Price that the Ornua PPI translates back to. We want to be paid per litre what the processor got paid per litre and if they want to pay a bonus on whatever grounds then they can pay it on top of that.

Latest Headlines

- Sections

Contact Us

Telephone

061 314 677

+353 61 314 677